Titolo completo

Minerals and the Lobito Corridor: Between Domestic Needs and the EU’s Derisking Strategy

|

Critical raw materials (CRMs) have become a key battleground between great powers. Countries need these resources to reach their industrial, energy, technological and military objectives. Underpinned by these sectors’ expansion, global CRMs demand is expected to rise drastically. Among such sectors, clean energy and decarbonisation efforts will be key drivers for demand growth. Clean technologies, such as solar, wind and batteries, are, indeed, much more mineral-intensive than their alternatives.[1]

However, countries and companies have increasingly focused on ‘derisking’ mineral supply chains, which are characterised by an extraordinarily high degree of geographical concentration along the entire value chain.[2] In these efforts, stakeholders at large need to manage geological factors combined with industrial, technological and infrastructure capabilities. Meanwhile, mineral-rich countries are considering strategies to seize geopolitical and economic benefits of this new rush while hedging between competing powers and without falling into a renewed resource curse. Against this backdrop, cooperation among mineral-rich and importing countries is essential to ensure adequate supply and prevent price spikes and instability. Such cooperation cannot be limited only to extraction, but it needs to span the entire value chain, including key infrastructure.

An illustrative example is the Lobito Corridor, which is deemed to unlock critical minerals potential located in the Democratic Republic of Congo (DRC) and Zambia and connect these countries to the international markets – especially the US and Europe – through Angola’s port.[3] The European Commission and Italy are key partners in this project.[4] In supporting it, the EU and Italy need to ensure that the Lobito Corridor generates a wide range of benefits not only to the international partners and markets, but especially for the local communities by addressing chronic problems through a holistic approach.

A challenging domestic dimension

The African countries involved in the Lobito Corridor (Zambia, Angola and DRC) face severe socio-economic challenges, notably a growing and young population, widespread poverty, political and security instability, and lack of energy access. The three countries have a combined population of almost 170 million,[5] a number that was less than half just 25 years ago, and the most recent UN projections indicate that their populations will double again by 2050.[6] Economically, these countries rank among the lowest globally in terms of GDP per capita, below the Sub-Saharan African (SSA) average (1,800 dollars), with Angola being the only partial exception, and well below the global average (approximately 15,000 dollars).[7] Consequently, national governments will be called and pressured to improve economic conditions, also by converting mineral wealth into tangible economic gains for their citizens. This need is further challenged by a particularly multifaceted set of issues, including heavy debt burden, security-related issues, especially in the Eastern DRC, alongside widespread governance problems including weak state capacity to enforce laws, corruption and political instability.[8]

Furthermore, these countries face chronic energy challenges, notably a lack of energy access.[9] This issue has been a historical feature of SSA and its socioeconomic troubles. Despite policy commitment and international support, energy access expansion in many SSA countries has often been outpaced by the population growth rate. As of today, 585 million people in SSA are still without a reliable connection to electricity networks. At the country level, in Zambia and Angola, the share of the population with access to electricity is 51.1 per cent, while in the DRC the situation is even more serious, with only 22.1 per cent of the population having access to electricity.[10] This equates to nearly 114 million people without access in the three countries. Beyond social implications, substantial energy deficits undermine mining activities and ambitions.[11] Furthermore, even when energy access is in place, mining ambitions are hindered by the instability of the system and excessive costs. Meanwhile, despite being small energy-consuming countries, they are all experiencing the effects of climate change disproportionately, recording more intense and frequent negative weather episodes, threatening key economic activities, such as agricultural and mining, and the livelihoods of the poorest segment of the population. Such difficult conditions may pose additional challenges to mines and mineral supplies and will further stress the limited state resources dedicated to adaptation measures.[12]

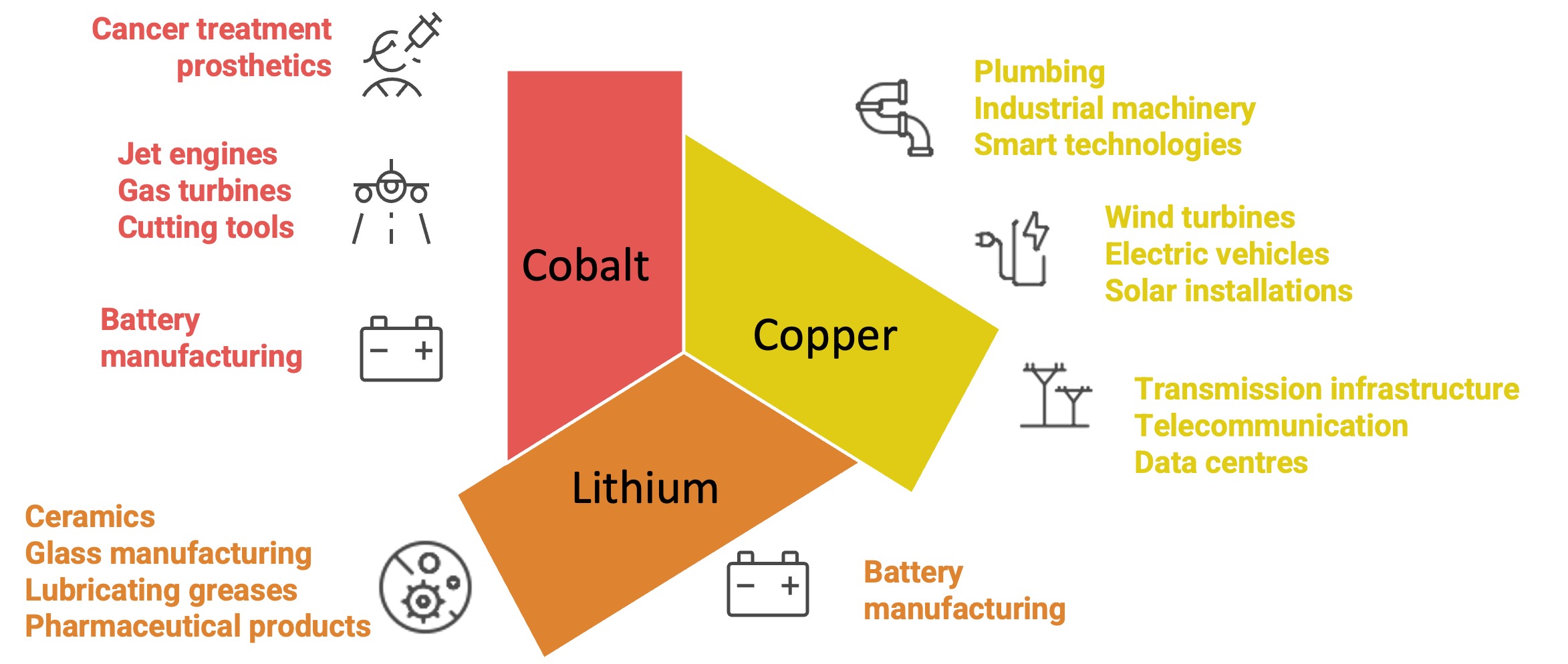

Paradoxically, beneath the poverty lies an extraordinary wealth of CRMs, necessary for a global green transition that aims to mitigate those very climate impacts (Figure 1).

Figure 1 | CRMs input for key industrial and clean tech uses

Source: Authors’ elaboration.

The local mining sector: Challenges and needs

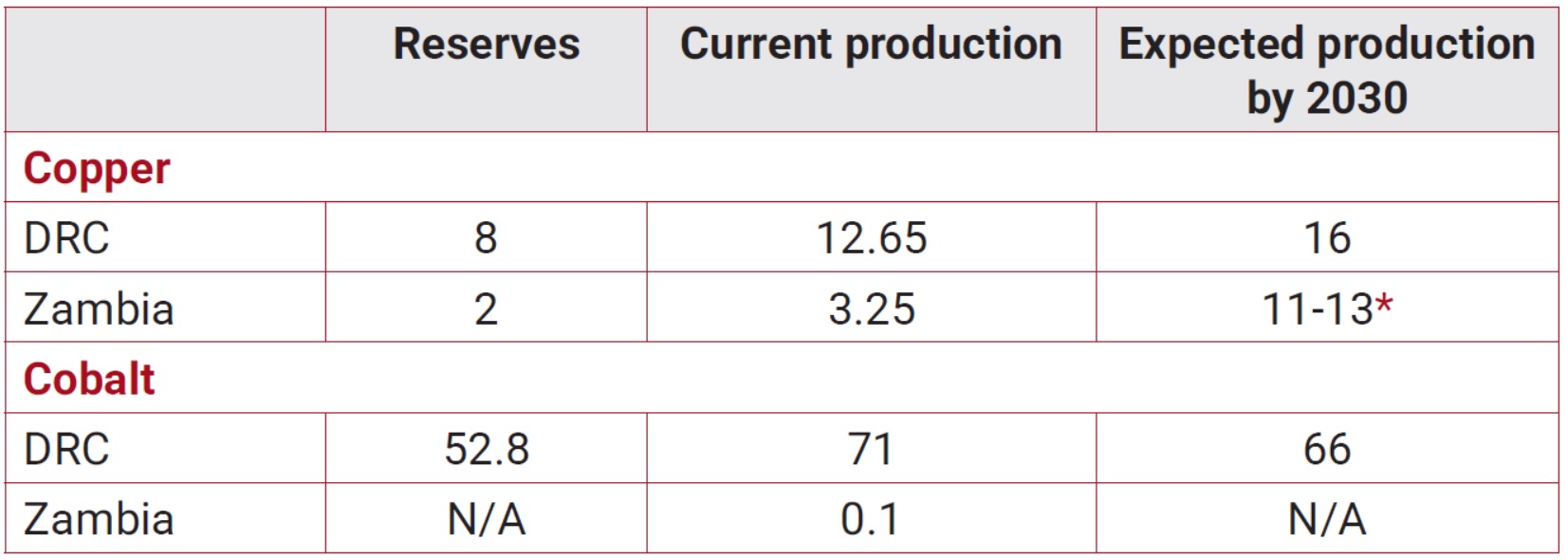

The surging global demand for these technologies has driven their economic value to historic highs, potentially offering a pathway out of the region’s socio-economic crisis. Indeed, Zambia and the DRC possess immense mineral reserves, mainly of cobalt, lithium and copper, although not evenly distributed. Zambia and the DRC are naturally rich in mineral resources; differently, Angola has vast reserves of oil and gas, though within the context of the Lobito Corridor, its role is mainly to serve as a gateway port to ship and transport resources to Western markets.

The number of resources and mining production of Zambia, and especially the DRC, is particularly staggering. Both current and future projections of copper and cobalt production showcase the importance of these countries in the global market (Table 1). By contrast, lithium is yet to be fully developed, despite large proven reserves, especially in the DRC. The DRC may become a relevant lithium producer as production from its Manono lithium deposit, estimated at over 130 million tonnes, is considered to be one of the largest in the world,[13] and is expected to begin as early as mid-2026,[14] although the project has faced several operational and governance challenges that could affect this timeline.[15]

Table 1 | Copper and cobalt as global shares in DRC and Zambia (%)

*Note: Authors’ calculation on the national strategy and market prediction provided by the IEA and by Zambia Ministry of Mines and Minerals Development, 2024.

Source: Authors’ elaboration on Canada Government, AfDB and IEA data.

Despite its vast mineral potential and despite offering a high mineral value-to-exploration-spending, Africa continues to attract a disproportionately small share of global exploration investment, receiving just 10.4 per cent of global spending in 2024.[16] Investment flows are subject to extreme price volatility and unexpected political developments, which have repeatedly disrupted investment timelines, while the unpredictability of the policy landscape, particularly the risk of resource nationalism, further deters foreign capital. Yet the geological fundamentals of the region remain compelling enough to attract growing interest; the DRC and Zambia, for instance, lead the continent in exploration capital, suggesting some investor confidence in the viability of their deposits.[17]

Nonetheless, the question of who benefits from these investments is equally important. SSA countries often are bound to accept non-profitable or inequitable long-term deals in exchange for short-term economic relief and immediate resources. The internal pressure to spend on immediate aid and development for the local population is high, and the available capital on the market comes at very high rates for SSA countries. This situation leads to an exchange of natural resources, through concessions or long-term leases, for short-term financial gains or unlocking of immediate resources for development investments.

A striking example of this concern is the Sino-Congolais des Mines (Sicomines) agreement signed in 2007 between the DRC and China. Under this resource-for-infrastructure model, China committed to investing approximately 3 billion dollars in infrastructure in exchange for Chinese firms gaining mining rights to mineral deposits valued at 93 billion dollars.[18] The Sicomines agreement is emblematic of a broader trend: through a series of similar deals and direct investments, Chinese firms have come to own or hold stakes in 15 of the largest copper and cobalt mines in the DRC, operating nearly 70 per cent of its industrial cobalt mines.[19] Although not as dire, the situation in Zambia is similar. Several mines, such as the Lumwana or Kansanshi, are owned by foreign companies, in these examples, Canadians.[20] Others instead are only partially owned by overseas companies, such as the Mopani mine, where the government-backed ZCCM-IH holds some shares but not the majority.[21]

Such an issue of ownership, coupled with the desire to seize economic opportunities, leads to a rising wave of resource nationalism, as governments increasingly recognise that minority stakes and royalty-based revenues leave the majority of profits in foreign hands, driving demands for greater state control over strategic mineral wealth. This dynamic of limited ownership and constrained revenues compounds a deeper structural problem. African countries endowed with vast critical mineral reserves risk becoming exporters of raw wealth rather than beneficiaries of it. To revert this trend, SSA countries need to develop regulatory, political, economic, and infrastructure capabilities to ensure operations generating added value in the country.

The mining sector is not limited to the upstream segment (i.e., extraction), it also encompasses the midstream and downstream activities, such as smelters and refineries, where raw minerals are processed. Mineral processing offers a pathway to domestic economic value addition. By processing CRMs, countries can benefit from higher export market prices, as processed materials have greater value than raw ores or concentrates. Additionally, mineral processing supports job creation, attracts downstream industries and strengthens national resilience within global supply chains.[22] Unfortunately, Zambia, and especially the DRC, deeply lack these stages of the value chains. The absence of refining plants results in the offshoring of the value-added part of the supply chain in third countries, mainly China, and leaves the African countries with a fraction of the value they could capture. Particularly telling is the situation in DRC, where, despite producing more than 70 per cent of the world’s cobalt, there are merely a handful of refineries, producing only semi-refined cobalt, and even their output production is negligible on the global scale.[23]

EU mineral diplomacy

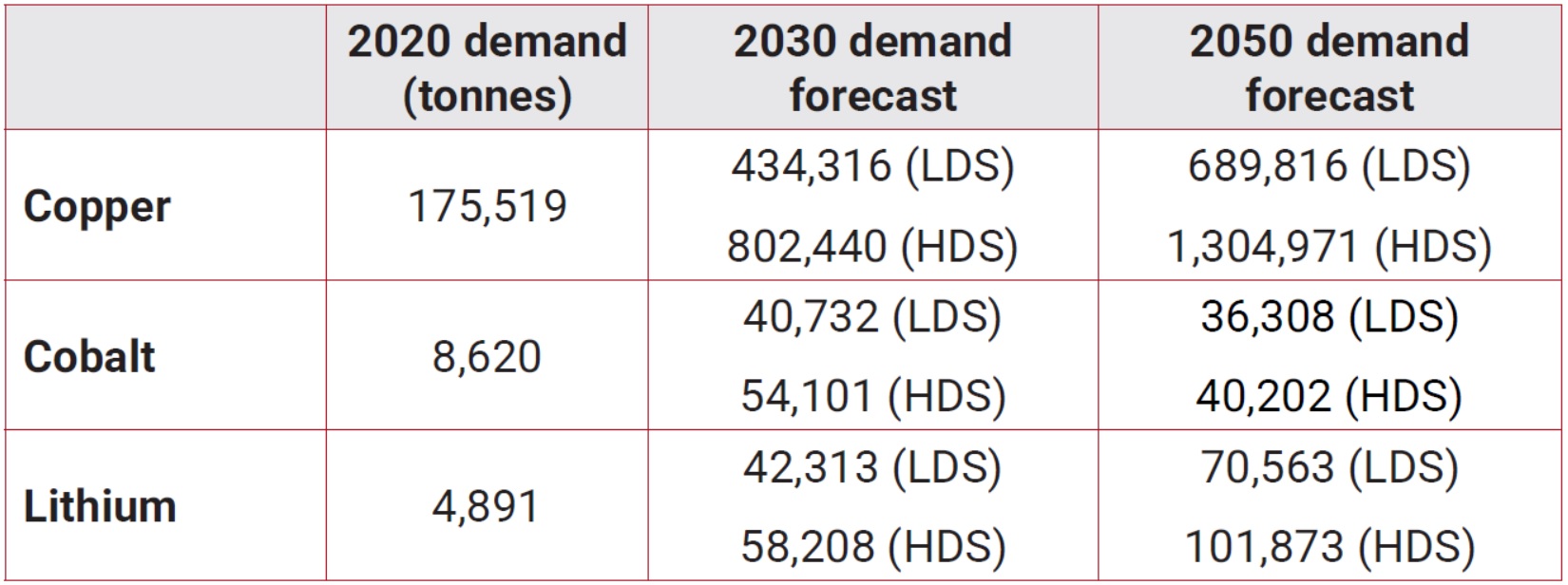

Against this backdrop, international stakeholders can support African countries and their economies in building new industries by avoiding an extractive approach. This new approach could be particularly beneficial also for the EU and its member states, including Italy, which need to carefully navigate the troubled waters of CRMs due to geopolitical competition, economic security concerns and local needs. In this effort, the EU can build on existing infrastructure projects that could have a multiplier effect on the local communities and the international community. Specifically, the European Commission, alongside Italy, Germany and France, has engaged with the Lobito Corridor through the Partnership for Global Infrastructure and Investment (PGII) launched by former US President Biden. The Corridor may help the EU in satisfying its growing demand for some of the critical minerals (Table 2). At the same time, security concerns have grown among European decision-makers given the risk of potential supply disruptions, price volatility and geopolitical risks.

Table 2 | EU demand forecasts for selected minerals

Note: LDS = Low demand scenario; HDS = High demand scenario.

Source: Carrara, Samuel et al., Supply Chain Analysis and Material Demand Forecast in Strategic Technologies and Sectors in the EU. A Foresight Study, Luxembourg, Publications Office of the EU, 2023, p. 10, https://data.europa.eu/doi/10.2760/386650.

To reduce these concerns, diversification is critical. Consequently, the EU has increasingly engaged with several African countries. In 2023, the Commission signed two separate MoUs with the DRC and Zambia on strategic partnerships related to CRMs.[24] While the political and economic arguments for deeper and positive EU-Africa cooperation are in place, concrete results are yet to materialise. The EU and European companies have struggled to keep pace with other players, notably the US, the Gulf and China, also due to lower acceptance of risks. Ideally, the development of the Lobito Corridor can be a building block of EU mineral diplomacy, as it could provide two benefits to improve the socio-economic situation of the African countries. Firstly, it will reduce the time of transport, hence lowering shipping costs and fast-tracking the supply chain, which can then supply higher quantities of minerals. Secondly, it can broaden the supply chain and bring benefits to the countries involved in the Corridor. Industries can be built all along the railway; it could create several intermediate refining steps from the raw to the final product, keeping the value-added components in the region.

However, the Corridor faces multiple challenges, as it is seen in competition with another critical infrastructure project, funded by China, TAZARA, while the US approach related to the project and to African partners is shifting as well. Therefore, it is critical for the EU, and Italy, to pursue this pathway, offering arrangements that place greater weight on economic value retention, environmental standards and engagement with local communities. To contribute to the creation of value-added industries in the African countries, the EU cannot overlook the chronic energy challenges faced by its partners. It is therefore of paramount importance that the EU’s mineral diplomacy is coupled with credible and concrete energy and climate finance to foster robust and decarbonised energy systems.[25] Whether Corridor development translates into lasting domestic gains will depend largely on the governance frameworks and partnership models that shape it. This is precisely the space into which Italy and the European Union have sought to position themselves, acknowledging the multiple dimensions of a successful mineral diplomacy. Now it is high time to translate these promises and aspirations into concrete results.

Pietro Rinaldi is Junior Researcher in the ‘Energy, climate and resources’ programme at the Istituto Affari Internazionali (IAI). Pier Paolo Raimondi is Senior Research Fellow in the ‘Energy, climate and resources’ programme at IAI and Research Fellow at the Florence School of Transnational Governance, European University Institute.

This brief is the third in a series produced in the framework of the research project “Italy at the forefront of infrastructure diplomacy: the Lobito Corridor case”, conducted by IAI with the support of the Italian Ministry of Foreign Affairs and International Cooperation, Fondazione CSF and Fondazione Compagnia di San Paolo. The views expressed herein are solely those of the authors.

[1] International Energy Agency (IEA), The Role of Critical Minerals in Clean Energy Transitions, Paris, IEA, May 2021, https://www.iea.org/reports/the-role-of-critical-minerals-in-clean-energy-transitions.

[2] Raimondi, Pier Paolo, “EU and Italian De-risking Strategies for Energy Transition: Critical Raw Materials”, in IAI Papers, No. 25|09 (June 2025), https://www.iai.it/en/node/20282.

[3] Lunardini, Marianna and Darlington Tshuma, “The Lobito Corridor and Africa’s Development Agenda: Synergies with the Mattei Plan and Global Gateway”, in IAI Briefs, No. 26|01 (January 2026), https://www.iai.it/en/node/21440.

[4] Lunardini, Marianna and Filippo Simonelli, “What Role for Italy’s Infrastructure Diplomacy? Lessons from the Lobito Corridor”, in IAI Briefs, No. 26|05 (February 2026), https://www.iai.it/en/node/21523.

[5] Zambia is home to 21 million people, Angola 38 million and the DRC has 109 million.

[6] UN Department of Economic and Social Affairs Population Division, World Population Prospects 2024, https://population.un.org/wpp.

[7] Lowest globally in terms of GDP per capita: Angola, 2,700 dollars; Zambia, 1,500 dollars and the DRC, 800 dollars. See IMF DataMapper, GDP per Capita, Current Prices: Zambia and Sub-Saharan Africa, 2026, https://www.imf.org/external/datamapper/NGDPDPC@WEO/ZMB/SSA.

[8] Isser, Deborah Hannah et al., “Governance in Sub-Saharan Africa in the 21st Century: Four Trends and an Uncertain Outlook”, in World Bank Policy Research Working Papers, No. 10713 (2024), https://hdl.handle.net/10986/41149.

[9] Bacon, Robert W. and Masami Kojima, Energy, Economic Growth, and Poverty Reduction. A Literature Review, Washington, World Bank, 2016, https://documents.worldbank.org/en/publication/documents-reports/documentdetail/312441468197382126.

[10] World Bank Data, Access to Electricity (% of Population), https://data.worldbank.org/indicator/EG.ELC.ACCS.ZS.

[11] Johansson, Daniel, “The Energy Crisis in Zambia Is Undermining the Lobito Corridor’s Potential — And DFC’s Investments”, in Energy for Growth Hub Blog, 16 April 2025, https://energyforgrowth.org/?p=7094.

[12] Hill, Matthew and Taonga Mitimingi, “Key Congo Copper-Export Route Cut Off After Bridge Collapses”, in Bloomberg, 2 March 2026, https://www.bloomberg.com/news/articles/2026-03-02/congo-s-main-copper-export-route-cut-off-after-bridge-collapses.

[13] African Development Bank, “Lithium”, in Critical Mineral Insights, No. 4 (16 October 2025), https://www.afdb.org/en/node/87893.

[14] Mishra, Shree, “Zijin Mining to Start Initial DRC Lithium Production in June”, in Mining Technology, 12 February 2026, https://www.mining-technology.com/?p=704792.

[15] European Resource Mining Community, Manono: Nine Red Flags in the Nascent Lithium Sector in the DRC, 8 December 2025, https://eurmc.org/?p=3056.

[16] Baskaran, Gracelin, “Underexplored and Undervalued: Addressing Africa’s Mineral Exploration Gap”, in CSIS Commentaries, 9 May 2025, https://www.csis.org/node/116220.

[17] DRC, 2025 Investment Climate Statements: Democratic Republic of the Congo, September 2025, https://www.state.gov/reports/2025-investment-climate-statements/democratic-republic-of-the-congo.

[18] Baskaran, Gracelin, “A Window of Opportunity to Build Critical Mineral Security in Africa”, in CSIS Commentaries, 10 October 2023, https://www.csis.org/node/107615.

[19] Economist, “How America Plans to Break China’s Grip on African Minerals”, in The Economist, 28 February 2023, https://www.economist.com/middle-east-and-africa/2023/02/28/how-america-plans-to-break-chinas-grip-on-african-minerals; Khan, Zahra, “Congo’s Cobalt Conundrum”, in Chemistry World, 19 June 2025, https://www.chemistryworld.com/news/4021696.article.

[20] Natural Resources Canada, Canadian Mining Assets, January 2026, https://natural-resources.canada.ca/minerals-mining/mining-data-statistics-analysis/minerals-mining-publications/canadian-mining-assets.

[21] International Resources Holding, IRH Completes the Official Acquisition of Mopani Copper Mines in Zambia, 7 March 2024, https://www.irh.ae/?p=8078.

[22] Pickles, Sophia, “Value Addition in the Context of Mineral Processing”, in Heinrich-Böll-Stiftung E-Papers, November 2023, https://www.boell.de/en/2023/11/15/value-addition-context-mineral-processing.

[23] African Development Bank, “Cobalt”, in Critical Mineral Insights, No. 3 (16 October 2025), https://www.afdb.org/en/documents/critical-mineral-insights-cobalt.

[24] European Commission, Global Gateway: EU Signs Strategic Partnerships on Critical Raw Materials Value Chains with DRC and Zambia and Advances Cooperation with US and Other Key Partners to Develop the ‘Lobito Corridor’, 26 October 2023, https://ec.europa.eu/commission/presscorner/detail/en/ip_23_5303.

[25] World Bank, Repositioning Zambia to Leverage Energy Transition Minerals for Economic Transformation. A Roadmap, Washington, World Bank, May 2025, https://hdl.handle.net/10986/43254.