Titolo completo

Europe’s Twin Dependencies: Building Energy and Digital Autonomy in a Fragmented World

|

The return of the Trump Administration has led to a resurgence of the idea of European “strategic autonomy” and “technological sovereignty”.[1] While the EU has developed regulatory tools and diversified some supply chains, structural gaps in energy infrastructure and digital capabilities continue to constrain action. Clean energy and computational power, i.e. the twin engines of 21st century economies, share fundamental characteristics that demand a unified strategic approach.[2] Both sectors exhibit steep learning curves, network effects and infrastructure lock-in that create path dependencies and competitive advantages for early movers.[3] Both face similar trade-offs between centralised control and distributed resilience, and both serve dual civilian and security functions. President Donald Trump’s aggressive use of tariffs as leverage and his push for deregulation, both domestically and abroad, presents Europe with a choice: whether to maintain economic openness while closing competitiveness gaps, or compromise a rule-based approach in pursuit of short-term trade gains. This brief analyses how the EU can strengthen its position in these strategic sectors through coherent industrial policy, targeted regulatory adaptation, international cooperation and enhanced institutional capacity.

The strategic economics of energy and compute

Energy and computational capacity (known as “compute”) represent the foundational inputs to modern economic and geopolitical power. Just as coal and steel defined the early industrial-era great power competition and accesso to hydrocarbons became geopolitically critical from the mid-20th century onwards, energy infrastructure and AI compute capabilities are increasingly central to 21st-century strategic rivalry. Four structural properties – learning effects, network externalities, a centralisation-resilience trade-off, and dual-use strategic value – shape both sectors and explain Europe’s exposure.

Learning effects generate first-mover advantages that compound over time: solar photovoltaic (PV) costs have fallen by approximately 90 per cent since 2010,[4] and the cost of AI training and inference has declined at comparable rates, with each doubling of cumulative deployment reducing unit costs further.[5] China’s dominance in solar panel manufacturing and the United States’ leadership in frontier AI models both reflect the learning-by-doing advantages accumulated through early, large-scale deployment rather than subsidy alone.[6]

Network effects and infrastructure lock-in reinforce this dynamic: Nvidia, the US chip giant, has built a tightly integrated ecosystem spanning its proprietary computing platform (which allows software to harness the power of Nvidia graphics processors for AI), cloud platform ecosystems, and grid-level energy storage systems. These components exhibit strong complementarities that make switching prohibitively costly.[7]

The centralisation-resilience trade-off adds a further constraint, since distributed architectures offer greater security against geopolitical coercion, but sacrifice the economies of scale that accelerate progress down the learning curve.

Finally, both sectors serve dual civilian and military purposes – from Starlink-equipped drones in Ukraine to the US semiconductor export controls weaponised against China – which intensifies geopolitical competition and limits the effectiveness of purely market-based solutions.[8]

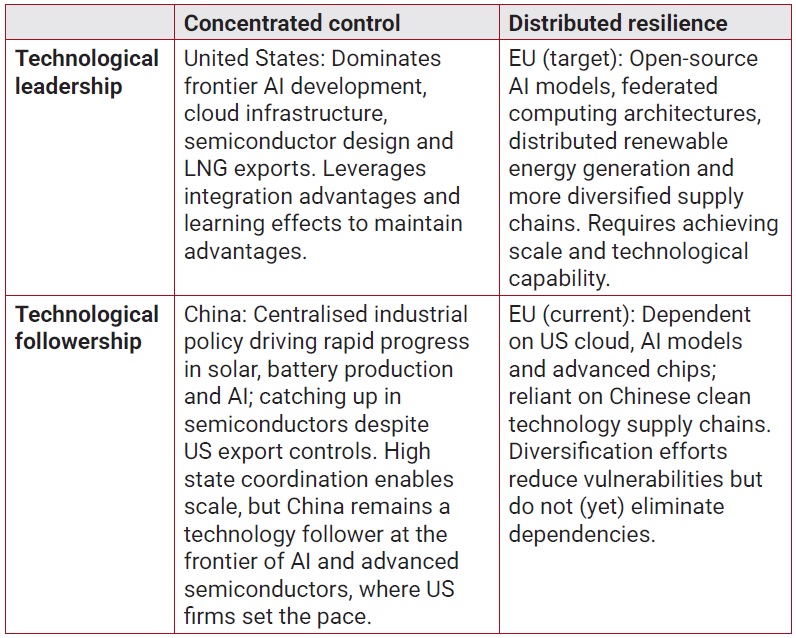

Applying this framework to Europe’s current position explains why challenges to strategic autonomy are persistent (Table 1). In solar manufacturing, European firms largely exited the market as Chinese competitors realised cost reductions by moving down the learning curve. In AI, European firms lag in developing frontier models, lacking both the computational infrastructure and the integrated tech ecosystems that characterise US and Chinese leaders. Similarly, European firms’ reliance on US cloud platforms and software for AI development constitutes a structural dependency. Dual-use dynamics further complicate any autonomy effort: security concerns push toward transatlantic integration, while competitiveness considerations pull toward maintaining open trade and technology flows with China.

Table 1 | Concentrated control vs distributed resilience

Note: The matrix maps current positions and, for the EU, strategic target positions across two axes: degree of control/distribution and technological leadership.

The EU Chips Act and AI gigafactory plans are necessary responses to this position, but the threshold for genuine strategic autonomy, encompassing home-grown capabilities at sufficient scale to provide credible alternatives during disruptions, lies above what current initiatives can achieve.

Challenges and goals in the energy system

The EU’s goal of becoming climate-neutral by 2050 requires a major restructuring of the entire European energy sector. Switching to climate-friendly, but naturally volatile sources of electricity generation, such as wind and solar power, requires significant investment in energy infrastructure, particularly in grid and storage capacities to balance out fluctuating electricity supply. For the period 2022-2030, the European Commission estimates that the EU will need to invest a cumulative total of 584 billion euros in the grid, a sum similar to that required for new generation capacities.[9] Moreover, achieving climate neutrality also requires the decarbonisation of final energy consumers, primarily through investment in electricity-based technologies, which will impose a significant cost burden on industries and private households.

From the perspective of autonomy goals, the trend towards decarbonisation is a double-edged sword. In the long term, it has the potential to strengthen Europe’s geoeconomic bargaining power by reducing dependence on external energy provision and creating new EU-led global markets through green standards and carbon pricing. However, during the transition to this state, a combination of traditional and new forms of external dependency leaves Europe exposed to a variety of risks in the international supply chain. This applies not only to reliance on natural gas as a bridge technology, but also to the resources needed to manufacture hard-to-substitute green technologies, which mostly comprise mineral raw materials and skills. Addressing these risks requires policymakers to adopt a supply chain approach.

This fact was recognised by the European Commission in its 2022 RePowerEU Strategy.[10] In response to Russia’s attack on Ukraine and the subsequent energy crisis, the strategy aims to decouple completely from Russian energy sources, accelerate domestic renewable deployment, diversify trade routes, and set targets for the domestic manufacture of heat pumps and PV modules. The strategic logic underpinning RePowerEU, namely reducing acute dependencies through supply chain diversification and domestic industrial capacity, has since become a template for EU responses to broader geopolitical disruptions. The trade tensions and technology competition intensifying from 2025 onwards have prompted analogous policy instruments, from the Net-Zero Industry Act to the Critical Raw Materials Act, as discussed below. In short, external shocks increasingly drive European industrial and supply chain policy.

Current autonomy policies in the field of energy

The EU’s current policies aim to support investments in renewable energy sources as a means of ending dependence on external fossil fuels. One major instrument is the Renewable Energy Directive (RED III), which sets general and sector-specific targets for the minimum shares of renewables in energy consumption.[11] By setting specific sub-targets for the use of renewable hydrogen in transport and industry, RED III also aims to promote the expansion of electrolytic hydrogen production. Moreover, the EU provides direct revenue support for domestic renewable hydrogen producers through the auctioning of production premia within the framework of the European Hydrogen Bank.

Apart from pushing for the faster deployment of renewable energy, the EU is paying increasing attention to the supply chain resilience of clean technologies. This is most evident in regulatory initiatives such as the 2024 Critical Raw Materials Act (CRMA)[12] and the Net-Zero Industry Act (NZIA).[13] CRMA sets out measures to diversify supply channels for mineral raw materials that are considered critical due to high import dependency and low technological substitutability, with a particular focus on materials used in clean energy technologies. NZIA aims to increase domestic manufacturing capacity for net-zero technologies. The set of policy instruments in both initiatives is similar. They mainly consist of reducing administrative (permit granting procedures) and financial (public funding streamlining) bottlenecks for prioritised investment projects. In the case of the NZIA, the aim of the resilience criteria for public procurement and the domestic support mechanism is to reduce dependencies on dominant foreign suppliers, particularly China in solar and battery manufacturing.

This cross-sectoral governance is complemented by initiatives to scale up specific clean technologies, such as the Industrial Carbon Management Strategy and the Battery Booster Strategy. The proposal for an Industrial Accelerator Act, particularly its provisions on local (i.e. European) content rules for clean energy technologies,[14] is a notable addition to policy interventions in favour of domestic clean technology manufacturing.

Although the EU is striving for more domestic content, it does not consider energy autarky a realistic long-term target. Strategic partnerships on energy and raw materials have emerged as a means of establishing new joint green supply chains while avoiding the high negotiation costs associated with traditional trade agreements.[15] These actions are financially supported by the Global Gateway Initiative, a programme that channels external infrastructure support to areas with high supply potential for Europe’s twin transformation.[16]

In sum, the EU’s supply chain perspective on strategic autonomy in the energy field is already very ambitious in scope. However, the broad scope is at odds with the limited impact of current measures.

AI and compute challenges

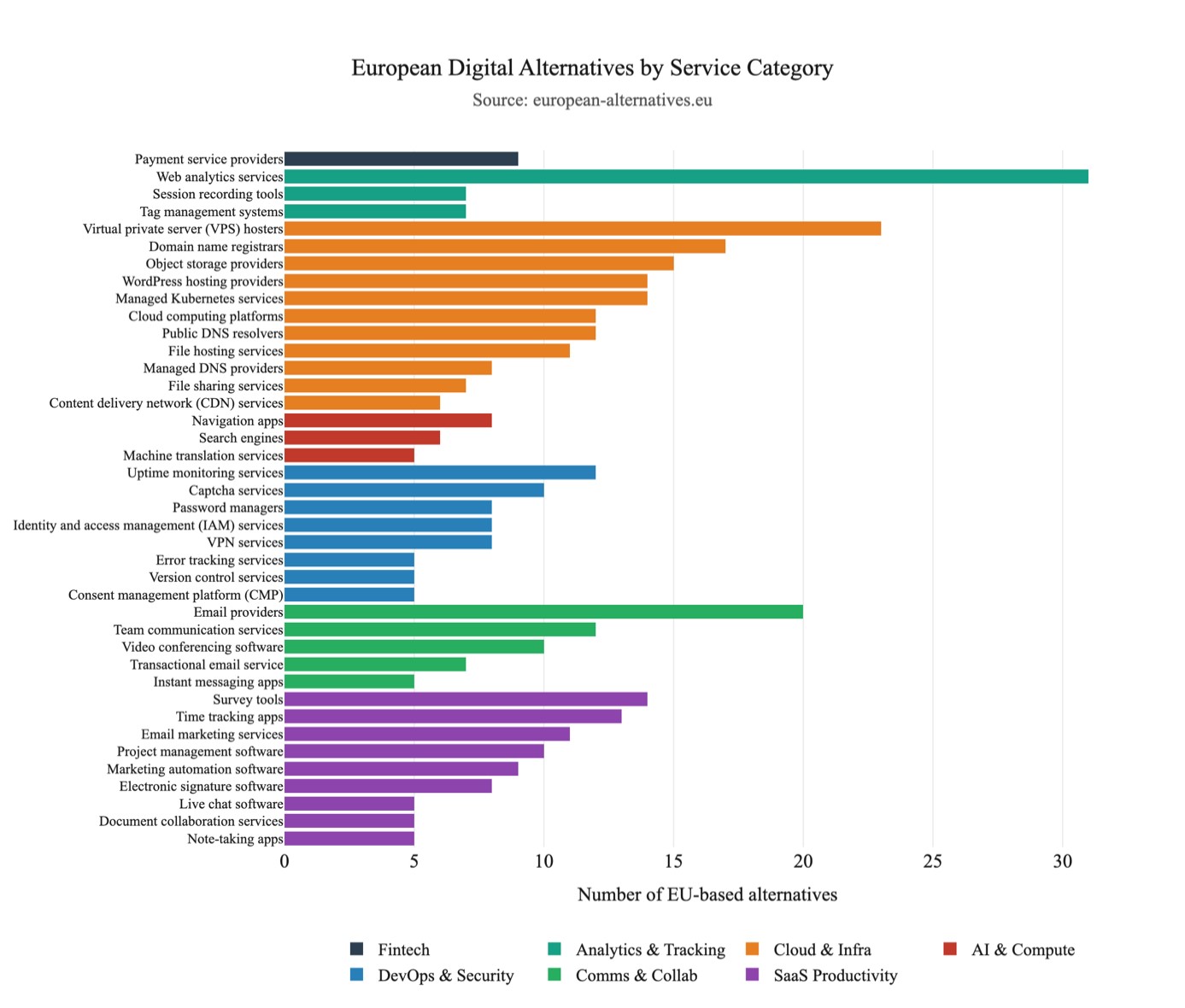

Similarly, Europe’s digital infrastructure deficit reflects its market position, but it is also shaped by the structural features through which AI and computing ecosystems develop. To analyse this deficit empirically, we draw on two complementary data sources: “European-Alternatives.eu”, a tracker covering 61 digital service categories, and “Europeantechmap.eu”, which tracks European tech companies across member states and sector classifications, both accessed via web scraping in March 2026.[17]

“European-Alternatives.eu” lists a total of 464 EU-based products and services across all 61 categories, with an average of 7.6 alternatives per category (Figure 1). However, these headline figures mask a stark internal divide. The eight categories classified as AI & Compute – covering generative AI, machine translation, web browsers, desktop operating systems, map APIs (which facilitates interaction among map services), search engines, spelling and grammar tools, and Function-as-a-Service platforms – have an average of just 4.1 EU-based alternatives compared to 8.1 for all other domains. While the difference may seem modest, many of these categories are effectively winner-take-most markets, where one or two providers set the de facto standard. In contrast, for cloud infrastructure and analytics, where European providers average 10-15 alternatives per category, the market is quite contested. For AI-facing services, however, it is not.

Figure 1 | Number of EU-based alternatives by service category

Source: european-alternatives.eu; own calculations.

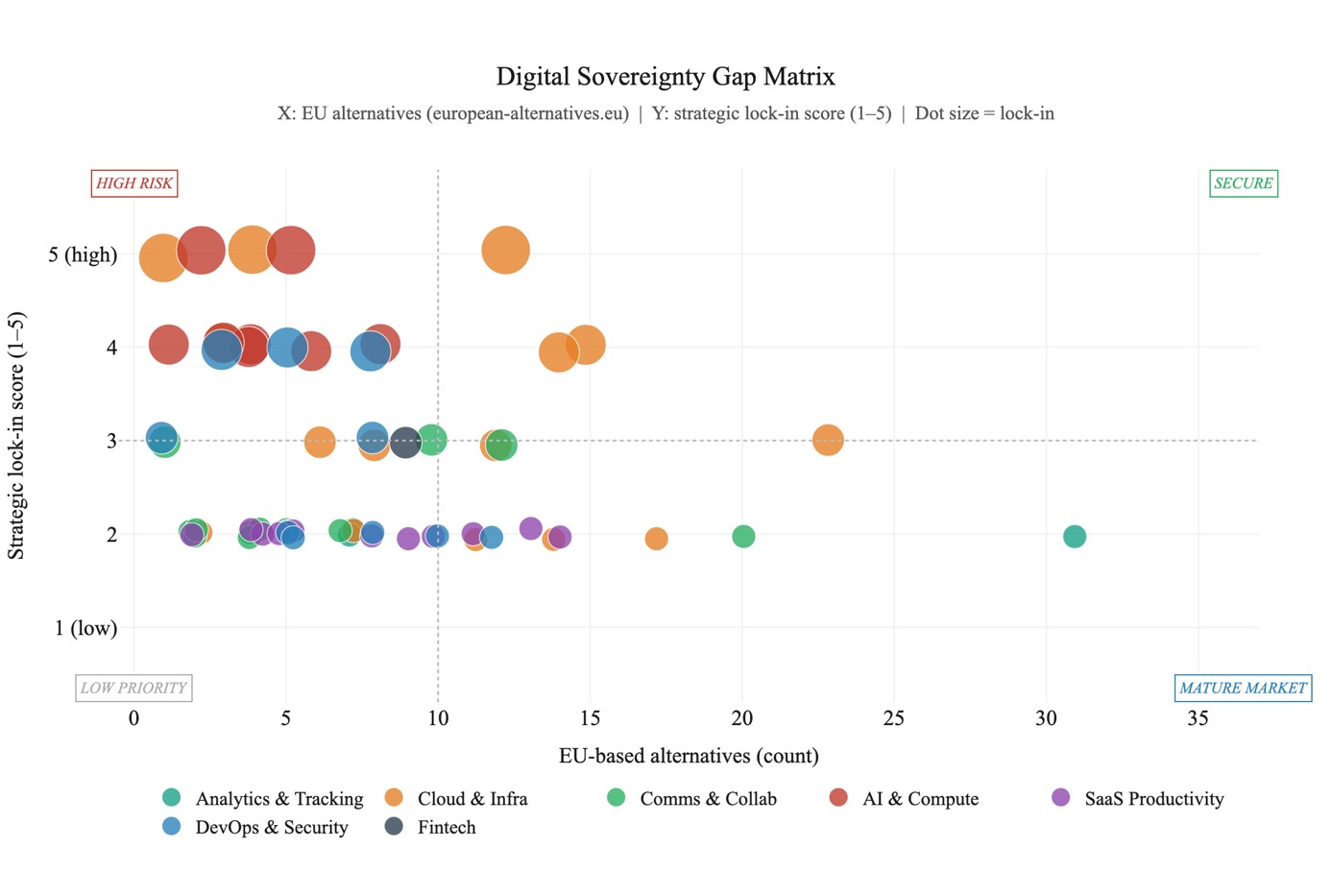

To assess lock-in potential, we assign each service category a strategic importance score on an ordinal scale of 1–5. This score captures four dimensions associated with structural lock-in: exposure to learning-curve effects, network externalities, switching costs, and dual-use relevance (Figure 2). Each dimension was scored independently and then aggregated.

Seven of the twelve service categories that fall into the high-risk quadrant, defined as a strategic lock-in score of 4 or above and six or fewer EU-based alternatives, belong to the AI & Compute domain. The remaining five are spread across cloud infrastructure and software development tooling, reflecting the broader digital stack dependencies that AI workloads rely on. In contrast, the secure quadrant (high lock-in, many alternatives) contains just three categories for Europe, all of which are in cloud infrastructure. This means that the categories where the strategic stakes are highest are precisely those where domestic supply is thinnest. This is a structural outcome of the learning-curve and network-effect dynamics described above: the same mechanisms that make these markets strategically important also make them resistant to entry.

Figure 2 | Relationship between strategic lock-in score and number of EU-based alternatives by service category

Source: european-alternatives.eu; own calculations.

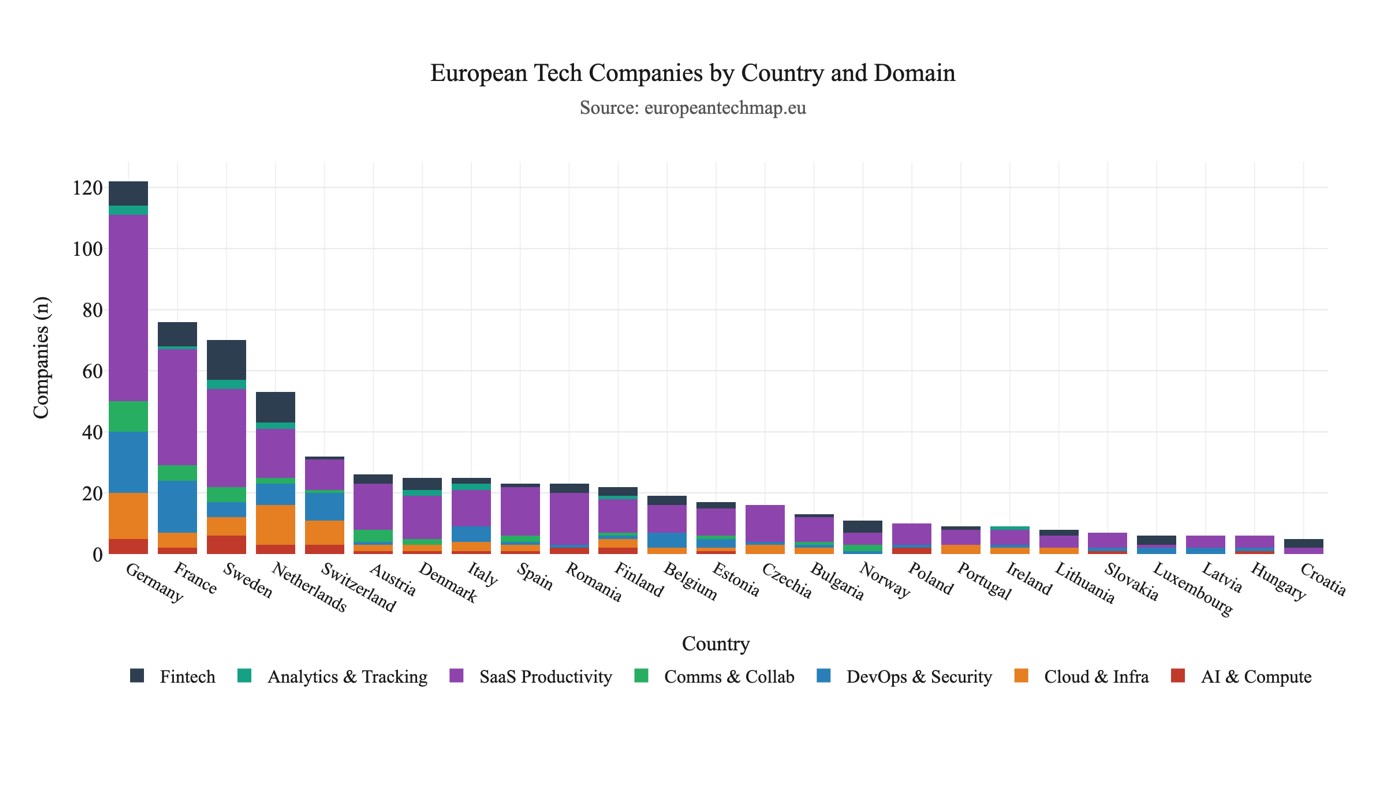

Of the 651 European tech companies tracked via “Europeantechmap.eu”, AI & Compute accounts for just 32 firms (4.9 per cent of the total). The vast majority of European tech activity – 329 firms, or roughly half of the total – falls under SaaS productivity, i.e. classic software tools with limited strategic lock-in, modest network effects and no meaningful dual-use dimension. In other words, Europe has successfully built a market for business software, but it has not built a market for AI infrastructure.

The geographic distribution of the 32 AI & Compute firms exacerbates this issue (Figure 3). Germany accounts for five, Sweden for six, Switzerland for three, and Finland and Romania for two each. Together, the top three countries represent 41 per cent of the entire European tech ecosystem, and the concentration is even more pronounced in AI. In 26 of the tracked countries, AI and compute firms account for less than 10 per cent of the national tech sector.

Figure 3 | Number of European tech companies by country and domain

Source: europeantechmap.eu; own calculations.

Two caveats are in order. Firstly, the datasets used here track presence rather than scale. Secondly, the AI landscape is evolving rapidly. What the data clearly establishes is that Europe’s digital dependency is concentrated in the AI and compute layer where future economic and strategic leverage will be determined.

Policy recommendations

• Introduce knowledge-focused local content rules for clean energy technologies. Many clean technologies are fixed-cost industries in which cost competitiveness derives directly from economies of scale. In markets where European producers hold small initial market shares, such as batteries, preferential treatment during the scale-up phase is warranted. Application of local content criteria should be limited to final products and key components with strong cross-industry spillover potential, with explicit exceptions for producers from countries engaged in green partnerships with the EU.

• Build a circular economy for critical raw materials to reduce import dependency. Recycling domestic stocks of critical raw materials, which are embedded in electronic waste such as batteries, reduces exposure to China’s dominance without requiring new import routes. The EU should extend binding minimum recycling quotas, on the model set by the EU Battery Regulation, to permanent magnets as the next priority.[18]Waste shipment rules should be tightened to prohibit exports of waste containing critical raw materials to non-members of the Organization for Economic Cooperation and Development (OECD).[19] Restricting exports to this club of countries serves a dual purpose: preventing the offshoring of critical material recovery to jurisdictions with weaker processing standards, and closing the regulatory gap that currently allows valuable secondary raw materials to leave the EU before they can enter domestic recycling.

• Expand risk-sharing instruments for energy-related outward FDI. The EU should refocus its Global Gateway Initiative on innovative support instruments for private investment in unexplored markets in developing economies. Support should include public equity as a risk buffer to attract private co-investors, and targeted insurance mechanisms to cover expropriation risk and the collapse of local institutions.

• Develop a strategic roadmap for energy and raw material partnerships. A strategic roadmap should begin by identifying which partner-country capabilities are most valuable and match each with the appropriate cooperation instrument. Cooperation should involve both financial and regulatory barriers.

• Fund a European Open Source AI Initiative with dedicated computing infrastructure. Europe cannot directly match the vertically integrated AI ecosystems of US hyper-scalers or the deployment scale of China’s state-directed approach. An alternative pathway exists through open-source foundation models and distributed innovation ecosystems that reduce vendor lock-in and align with European governance preferences.[20] The Commission should fund the development of open models under permissive licences, enabling European firms to fine-tune and deploy them independently of proprietary US platforms, supported by Europe-specific training datasets and small language models (SLMs). This strategy accepts a strong second-tier capability position rather than attempting frontier competition.

• Make European capability-building a precondition for any transatlantic digital coordination framework, and distinguish dialogue from rule revision. Dialogue between the EU and the United States is legitimate and overdue, as transatlantic friction over instruments such as the Digital Services Act has often rested on the misreading of the EU law: the DSA is a structural market regulation, not a censorship mechanism, and clarifying that distinction serves both sides. Where the United States interprets European digital rules as discriminatory trade barriers, the EU has both the standing and the obligation to correct the record. What should not be available for negotiation, however, is the content of democratically enacted legislation. This is acute in AI governance: if the EU weakens its AI Act commitments before establishing sufficient European open-source alternatives, it deepens structural dependencies while surrendering the regulatory leverage that gives European digital policy its weight. The correct sequence is capability first, coordination second, so that any joint framework on digital enforcement is negotiated between parties with independent options.

Competitiveness through capability

The Trump Administration’s aggressive unilateralism and deregulation have put significant pressure on the European economic model. The EU is increasingly tempted to protect its markets using similar political means. However, imitating foreign policies is the wrong approach when it comes to digital and energy technologies. The root cause of the EU’s high exposure to external policy risks is its lack of technological sovereignty. This cannot be remedied by raising tariff barriers or other short-term market interventions because it is caused by the fundamental characteristics of these technologies. Their tendency to exhibit strong learning curves, network effects and high switching costs gives technological frontrunners a crucial advantage. Overcoming external dependencies in these critical fields therefore asks for a consistent, long-term industrial strategy. Internally, this requires the EU to further harmonise and simplify regulatory frameworks, exploiting the potential of the single market as an engine for scaling innovative business models. Externally, the EU should adopt a pragmatic approach to cooperation. This should involve improving access to external knowledge and sales markets through long-term partnerships, while also strengthening defence instruments to reduce the risk of economic coercion.

Such a strategic shift will cause adaptation costs which put Europe’s commitment to unity to an even greater test. This is because these costs will fall unevenly across member states: countries with greater exposure to carbon-intensive industries, deeper trade ties with China, or higher dependence on US digital infrastructure will face more acute adjustment pressures than others. However, the consequences of inaction are likely to be more severe. This is because strategic autonomy in energy and digital domains is not merely an economic objective but a prerequisite for European political sovereignty. Moreover, the presence of learning curves, network effects and geopolitical competition means that Europe’s window for building autonomous capabilities is narrowing. The choices made in the next years will determine whether Europe retains agency in the 21st century’s defining strategic domains.

Anselm Küsters is Head of Division for Digitalisation and New Technologies at the Centre for European Policy (cep), Berlin. André Wolf is Head of Division for Technology, Infrastructure and Industrial Development at the Centre for European Policy (cep), Berlin.

This brief was produced in the framework of the research project “European strategic autonomy and the challenge of new green and digital technologies” supported by the Fondazione CSF and Fondazione Compagnia di San Paolo within the Geopolitics and Technology call. The views expressed in this report are solely those of the author.

[1] Renda, Andrea, “Leveraging Digital Regulation for Strategic Autonomy”, in FEPS Policy Briefs, March 2022, https://feps-europe.eu/?p=53756; Rone, Julia “‘The Sovereign Cloud’ in Europe: Diverging Nation State Preferences and Disputed Institutional Competences in the Context of Limited Technological Capabilities”, in Journal of European Public Policy, Vol. 31, No. 8 (2024), p. 2343-69, https://doi.org/10.1080/13501763.2024.2348618.

[2] Alcaro, Riccardo, “Running in Circles. How Europe’s Quest for Autonomy Has Turned into Higher Dependencies”, in Survival, Vol. 68, No. 2 (April-May 2026), p. 85-116, DOI 10.1080/00396338.2026.2647641. On energy-compute, see: Sastry, Girish et al., “Computing Power and the Governance of Artificial Intelligence”, in arXiv, 13 February 2024, https://doi.org/10.48550/arXiv.2402.08797; Azhar, Azeem, The Exponential Age. How Accelerating Technology Is Transforming Business, Politics, and Society, New York, Diversion Books, 2021.

[3] Nemet, Gregory F., How Solar Energy Became Cheap. Pathways to a Solar-Centric Economy, 2nd ed., London/New York, Routledge, 2026; Sevilla, Jaime et al., “Compute Trends Across Three Eras of Machine Learning”, in 2022 International Joint Conference on Neural Networks (IJCNN), 30 September 2022, DOI 10.1109/IJCNN55064.2022.9891914; Kaplan, Jared et al., “Scaling Laws for Neural Language Models”, in arXiv, 23 January 2020, https://doi.org/10.48550/ARXIV.2001.08361.

[4] International Renewable Energy Agency (IRENA), Renewable Power Generation Costs in 2023, Abu Dhabi, September 2024, https://www.irena.org/Publications/2024/Sep/Renewable-Power-Generation-Costs-in-2023.

[5] Maslej, Nestor et al., The AI Index 2025 Annual Report, Stanford University, 2025, https://hai.stanford.edu/ai-index/2025-ai-index-report.

[6] Nahm, Jonas and Edward S. Steinfeld, “Scale-up Nation: China’s Specialization in Innovative Manufacturing”, in World Development, Vol. 54 (February 2014), p. 288-300, DOI 10.1016/j.worlddev.2013.09.003.

[7] Küsters, Anselm and Matthias Kullas, “Competition at Risk in Generative AI Markets”, in cepInputs, No. 1/2026 (20 January 2026), https://www.cep.eu/eu-topics/details/competition-at-risk-in-generative-ai-markets.html.

[8] Farrell, Henry and Abraham L. Newman, “Weaponized Interdependence: How Global Economic Networks Shape State Coercion”, in International Security, Vol. 44, No. 1 (Summer 2019), p. 42-79, https://doi.org/10.1162/isec_a_00351.

[9] European Commission, Implementing the RePower EU Action Plan: Investment Needs, Hydrogen Accelerator and Achieving the Bio-methane Target (SWD/2022/230), 18 May 2022, https://eur-lex.europa.eu/legal-content/en/TXT/?uri=celex:52022SC0230.

[10] European Commission, REPowerEU: Joint European Action for More Affordable, Secure and Sustainable Energy (COM/2022/108), 8 March 2022, https://eur-lex.europa.eu/legal-content/en/TXT/?uri=celex:52022DC0108.

[11] European Parliament and Council of the EU, Directive (EU) 2023/2413 of 18 October 2023 […] as Regards the Promotion of Energy from Renewable Sources, https://eur-lex.europa.eu/eli/dir/2023/2413/oj/eng.

[12] European Parliament and Council of the EU, Regulation (EU) 2024/1252 of 11 April 2024 Establishing a Framework for Ensuring a Secure and Sustainable Supply of Critical Raw Materials, https://eur-lex.europa.eu/eli/reg/2024/1252/oj/eng.

[13] European Parliament and Council of the EU, Regulation (EU) 2024/1735 of 13 June 2024 on Establishing a Framework of Measures for Strengthening Europe’s Net-Zero Technology Manufacturing Ecosystem, https://eur-lex.europa.eu/eli/reg/2024/1735/oj/eng.

[14] European Commission, Proposal for a Regulation on Establishing a Framework of Measures for the Acceleration of Industrial Capacity and Decarbonisation in Strategic Sectors (COM/2026/100), 4 March 2026, https://eur-lex.europa.eu/legal-content/en/TXT/?uri=celex:52026PC0100.

[15] Wolf, André, “Clean Trade and Investment Partnerships”, in cepInputs, No.10/2025 (29 April 2025), https://www.cep.eu/eu-topics/details/clean-trade-and-investment-partnerships.html.

[16] Wolf, André and Eleonora Poli, “The Trade Potential of Infrastructure Partnerships: The Case of EU Global Gateway”, in Central European Economic Journal, Vol. 11, No. 58 (2024), p. 380-405, https://ceej.wne.uw.edu.pl/?p=2116.

[17] For “European-Alternatives.eu”, we scraped all category landing pages to extract EU alternative counts and company names across the 61 service categories. For “Europeantechmap.eu”, we collected company-level entries, yielding 651 firms across 30 European states. Category assignments and deduplication were carried out programmatically.

[18] European Parliament and Council of the EU, Regulation (EU) 2023/1542 of 12 July 2023 Concerning Batteries and Waste Batteries, https://eur-lex.europa.eu/eli/reg/2023/1542/oj/eng.

[19] European Parliament and Council of the EU, Regulation (EU) 2024/1157 of 11 April 2024 on Shipments of Waste, https://eur-lex.europa.eu/eli/reg/2024/1157/oj/eng.

[20] Küsters, Anselm, Small Is Beautiful 2.0. Mit digitaler Dezentralisierung zu einer menschlicheren Wirtschaft, Freiburg, Herder, 2026.